TAX ADVISOR Offshore Companies Rental Tax Exposure

Category:

Real estate, Posted:19 Sep 2011 | 06:00 am

Over the past year we have been receiving a steady stream of inquiries from readers, agents and property owners about just what is the legal rental tax liability for owners who use an offshore holding company.

We spoke to the firm Phuket office of Duensing and Kippen who are tax and legal advisors who have given the following explanation –

"The use of off-shore entities, such as a company incorporated in the British Virgin Islands ("BVI") to own real estate is not uncommon in Thailand. One reason often cited by investors using such entities organized under foreign law for such purpose is that they believe it will result in significant tax savings. Whereas this may be true with regard to any tax applicable to the "sale" of the real estate by way of sale of the off-shore entity itself, it may not be true with regard to other potential tax liabilities. This article will analyze the tax consequences of an off-shore entity renting out real estate it owns in Thailand.

In general, juristic persons "carrying on business in Thailand" are subject to corporate income tax ("CIT") at the basic rate of 30%. CIT is applicable whether these entitles are incorporated under Thai law or some other foreign law. Entities organized under Thai law are subject to CIT on their worldwide income. However, entities organized under a foreign law are only subject to CIT if such income results from "carrying on business in Thailand".

If an entity incorporated under foreign law that is not "carrying on business in Thailand", but receives payment of assessable income from or within Thailand, such payment is subject to a withholding tax ("WHT") at a rate 10% or 15% depending on the type of payment, for example as follows:

INCOME DERIVED FROM: WHT RATE:

Service 15%

Interest 15%

Royalties 15%

Dividends 10%

Rent 15%

Liberal professions 15%

Where the recipient of assessable income is an off-shore party, the Revenue Code of Thailand ("RC") places the liability for filing the applicable WHT return and submitting the tax payment itself on the payer of the assessable income; in our rental income example, the lessee of the real estate owned by the off-shore entity.

Thus, tax liability for such rental income depends on whether or not the off-shore entity is deemed to be "carrying on business in Thailand". The RC does not define "carrying on business in Thailand". Section 66, paragraph 2 of the RC states that juristic companies or partnerships organized under foreign laws and carrying on business in Thailand are subject to the same tax as those organized under Thai law, but only with respect to income arising from or in consequence of the business carried on in Thailand. In addition, Section 76bis of the RC states:

"For a company or juristic partnership incorporated under foreign laws which has an employee, an agent or a go-between for carrying on business in Thailand and as a result receives income or profits in Thailand, such company or juristic partnership shall be deemed to be carrying on business in Thailand and the person who acts as an employee, an agent or a go-between for the business, whether he is an individual or a juristic person, shall be deemed to be representative of the company or juristic partnership incorporated under foreign laws and shall have the duty and liability to file a tax return and tax payment in accordance with the provisions of this Part, with respect to only the abovementioned income or profits."

The practical implication of Section 76bis is obvious. If the real estate owned by a foreign entity is leased out through an on-shore agent, rental pool, etc., such agent or rental pool company could be deemed to be an "employee, an agent or a go-between" of such foreign entity. The result would be that the foreign entity would then be treated like a Thai entity with regard to the income derived from its real estate located in Thailand and its rental income would be subject to the same tax regime. Furthermore, the on-shore liability to file the tax return and pay the applicable tax on behalf of the off-shore entity would be on the said agent or rental-pool company.

It should be noted, however, that there are exceptions to the above. Depending on the jurisdiction in which such off-shore entity is registered such entity, and thereby any purported on-shore agent of the off-shore entity, may be able to invoke the provisions of a Double Taxation Agreement ("DTA") between the jurisdiction in which the off-shore entity was incorporated and Thailand, thus limiting the potential and scope of exposure to full Thai CIT on such rental income. Unfortunately, however, investors using off-shore entities from jurisdictions that do not have a DTA with Thailand such as the BVI, will not be entitled to invoke the protection. Both their off-shore entity and its on-shore agent have a significantly heightened exposure to full Thai CIT liability on rental income earned in Thailand."

As usual please seek professional advice on matters pertaining to legal and tax and make informed decisions.

Other News

Read more

New Phuket Hotel Market Update 2024 Report From C9 Hotelworks

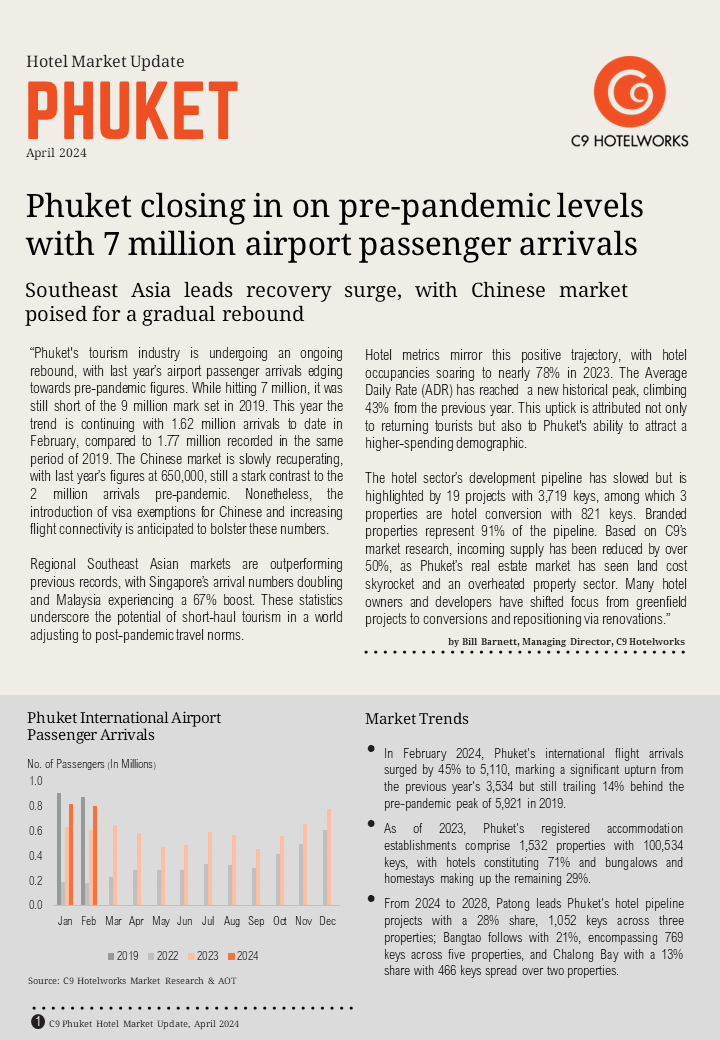

Category: Hotels|Tourism, Posted:17 Apr 2024 | 19:06 pm Phuket’s tourism industry is undergoing an ongoing rebound, with last year’s airport passenger arrivals edging towards pre-pandemic figures according to C9 Hotelwork’s Phuket Hotel Market Update 2024. While hitting 7 million, it was still short of the 9 million mark set in 2019. This year the trend is continuing with 1.62 million arrivals to date […]Read more