The Inside Story On Rental Income Taxation

Category:

Real estate, Posted:29 Jul 2011 | 06:00 am

One of the potentially contentious issues for the islands property sector in years ahead is Thailand's Revenue Department plugging the current hole in the dam on tax for rental income of villas and condo properties.

There remains a gray area between what is lawfully required and common practice but on the not too distance horizon compliance will without a doubt become a higher profile issue.

Talking to Phuket-based legal group Duensing Kippen, we have asked them out lay out exactly under existing legislation what tax liability exists –

"Many purchasers of real estate in Thailand are not using their newly purchased home as a permanent personal residence. Such assets are often meant to be used as a holiday home only and are unoccupied for the remainder of the year. One of the ongoing financial burdens of owning a holiday home is the common area fee. Such fee is usually connected to the ownership of such a holiday home and is payable even if the purchaser does not use his asset. In order to "cover the losses" or to receive a return of investment some purchasers are willing to rent out their holiday home for a limited time and therefore "earn" income from their asset. Such owners must be aware of the taxation issues connected to the lease income from such holiday home. This article will discuss the taxation of individuals who own real estate in Thailand and who receive rental income from renting out the property.

First of all, it is important to note that the duty to pay tax on rental income in Thailand does not depend on being a "tax resident" of Thailand or whether you receive the income in Thailand. This fact is often misunderstood. A tax resident of Thailand is "any person staying in Thailand for a period or periods aggregating 180 days or more (…)" (RC Section 41 ). However, rental income is considered taxable income in accordance with Section 40(5) of the Thai Revenue Code ("RC"). And RC Section 41 further states that "[a] taxpayer [i.e. "anyone"] who in the previous tax year derived assessable income under Section 40 (…) from a property situated in Thailand shall pay tax (…), whether such income is paid within or outside Thailand." Therefore, an individual, whether resident or non-resident, has to pay tax on lease income independent of whether the rental income is paid on-shore or off-shore.

Next, the taxable income needs to be defined. The RC allows certain deductions on rental income. According to Section 43 RC in conjunction with Section 5(1)(a) of the RC Royal Decree No. 11 ("RD") expenses may be deducted as follows "[i]n the case of houses, buildings, other constructions (…): if let by the owner, a standard deduction of 30 percent shall be allowed as expenses (…)". The emphasis is on the "owner". Please note that in the case of sub-leasing, and therefore in the common case of a lessee who is under a long term lease arrangement with a developer whereby such lessee is renting out such long term leased property, the 30% standard deduction is not applicable. In such a case, only the rent (pre-)paid to the developer can be deducted as an expense.

Another option for the tax payer to define the taxable income is to procure sufficient evidence of the tax payer's actual expenses. If these are higher than the standard deduction allowed necessary, then reasonable expenses shall be deductible. Note that restrictions on deductibility apply in accordance with the relevant regulations for corporate entities in Thailand.

The amount of tax payable is calculated on a progressive tax scale for personal income tax purposes as follows:

TAXABLE INCOME (BAHT) RATE

0 – 150,000 exempt

150,001 – 500,000 10%

500,001 – 1,000,000 20%

1,000,001 – 4,000,000 30%

4,000,001 and above 37%

The individual tax payer is required to report and remit his income tax using the personal income tax return form PND 91 by the end of March after the year in which the income was paid. Failure to report income can result in an assessment by the Revenue Department. The penalty is equal to the amount of additional tax payable. Further a surcharge of 1.5% per month on the tax payable is applicable.

Finally, it should also be noted that an "additional" category of tax is also payable each time the rent is paid. It is the duty of the payer of the rent who is renting the villa to deduct a "withholding tax" from the rental payment and submit it to the local Revenue Department. However, the owner and recipient of the rental payment is also jointly liable for such withholding tax payment. The amount of withholding tax depends on whether the owner is a tax resident of Thailand and also whether the payer of the rental is a juristic person or an individual. If the owner is not a tax resident of Thailand the withholding tax rate is 15%. The legal status of the payer does not matter if the owner is not a tax resident of Thailand. If the owner is a tax resident of Thailand and the payer is a juristic person, the withholding tax rate is 5%.

Please note that the withholding tax is not really additional taxation on the rental income, but merely a pre-payment of the personal income tax of the owner. The withholding tax will be credited against the final tax payment of the owner. However, if the withholding tax is not paid when the rent is paid, then the owner and recipient of the rental income is subject to significant penalty and surcharge payments."

Other News

Read more

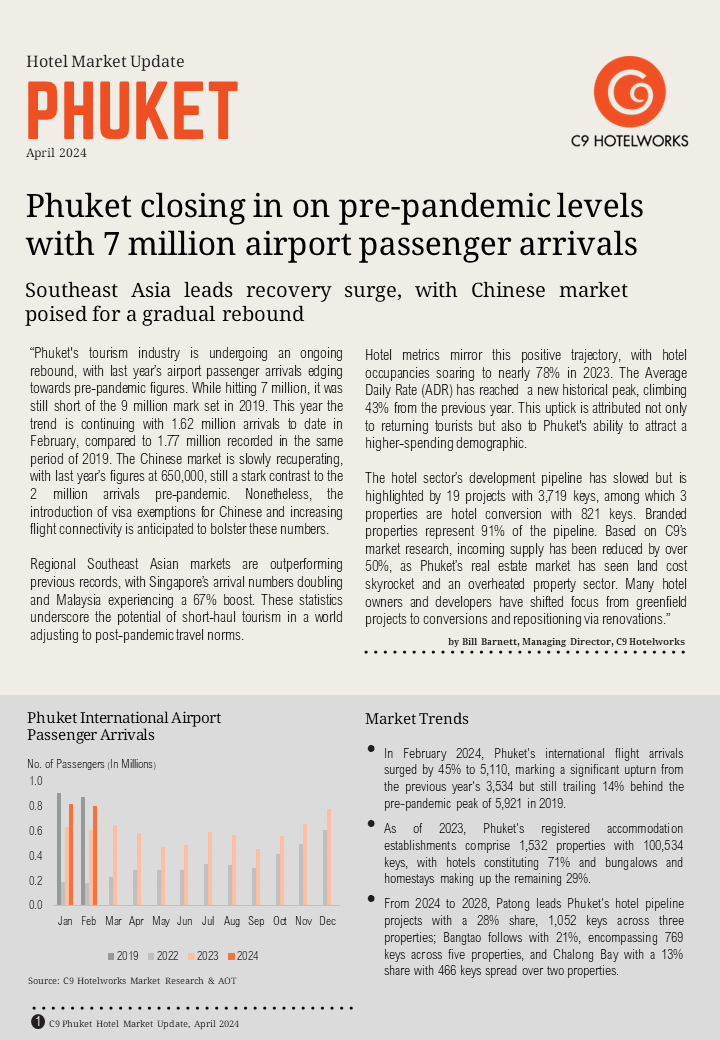

New Phuket Hotel Market Update 2024 Report From C9 Hotelworks

Category: Hotels|Tourism, Posted:17 Apr 2024 | 19:06 pm Phuket’s tourism industry is undergoing an ongoing rebound, with last year’s airport passenger arrivals edging towards pre-pandemic figures according to C9 Hotelwork’s Phuket Hotel Market Update 2024. While hitting 7 million, it was still short of the 9 million mark set in 2019. This year the trend is continuing with 1.62 million arrivals to date […]Read more