MYTHBUSTING Thai Corporate Tax Explained

Category:

Real estate, Posted:26 Feb 2012 | 14:13 pm

All too often investors come to our office after having read that Thai corporate tax is high and they start looking at offshore vehicile and other exotic tax planning elements.

With an update to Thailand's tax code which is now very competitive, it makes doing business in the country less burdensome.

We've asked a leading Phuket based tax and legal advisory DK (Duensing Kippen) to explain –

"After the elections there was a lot of discussion about the new government's plan to reduce the corporate income tax rates ("CITR"). While mostly the potential negative impact of the minimum wage rate increase on businesses in Thailand where publicly debated, the government actually went ahead and reduced the CITR significantly. Surprisingly relatively few people seem to be aware of this. Accordingly, please find in the following a summary of the recently enacted revised CITR.

Pursuant to Title II, Chapter 3, Schedule 2(a) of the Revenue Code ("RC") the CITR on profit for Thai companies is 30%. However, pursuant to Title I, Section 3(1) of the RC, this rate may be reduced for some or all such companies by way of the Cabinet issuing a "Royal Decree" ("RD").

And, in fact, under RD 471 (2008) the CITR for "small to medium enterprises" ("SME"s) defined there as companies who's total capitalization was THB 5,000,0000 or less on the last day of the tax year, was exempted for income not exceeding THB 150,000 and further reduced to 15% for taxable income between THB 150,001 to THB 1,000,0000 and to 25% for taxable income from THB 1,000,001 to THB 3,000,000. Also under RD 467 (2007) the CITR for companies listed on the Stock Exchange of Thailand ("SET") on the "market for alternative investment" ("MAI") was reduced to 20%, while the CITR for all other companies listed on the SET was reduced to 25%.

However, on 14 December 2011 the Cabinet issued RD 530 which repealed and replaced RD 471 and repealed and replaced Section 3(2) of RD 467. Accordingly, the CITR for SMEs, which are now defined as any company with a capitalization of not more than THB 5,000,000 on the final day of the tax year and which company does not have income exceeding THB 30,000,000 in that same tax year, is now as follows:

(1) exempted on net profit up to THB 150,000 for all of the following tax years which begin on or after 1 January 2012;

(2) 15% on net profit from THB 150,001 up to THB 1,000,000 for all of the following tax years which begin on or after 1 January 2012;

(3) 23% on net profit of THB 1,000,0001 or more for the tax year which begins on or after 1 January 2012; and

(4) 20% on net profit of THB 1,000,0001 or more for all of the following tax years which begin on or after 1 January 2013.

The CITR for all companies including those that are listed on the SET except for those which listed on the MAI on the SET is now for three consecutive accounting periods only as follows:

(1) 23% on net profit for the tax year which begins on or after 1 January 2012; and

(2) 20% on net profit for the following two tax years which begin on or after 1 January 2013.

The CITR for the companies that are listed on the MAI on the SET remains 20% on net profit under the portion of RD 467 which remains in effect.

In conclusion, these CITR reductions are clearly welcomed by those investing and doing business in Thailand. However, it should be noted that although as provided for under RD 530 the CITR reductions for SMEs are "permanent", they are not so for all other (non-MAI listed) companies. It is unclear, if it is "planned" to extend or even increase these reductions after the expiration of the reductions in three years.

The perhaps most commonly stated rationales for the CITR reductions is to make Thailand's business environment more competitive with its neighbors and further to "compensate" Thai companies for the coming minimum wage increases. But the reductions are not "permanent" for most "normal" companies under RD 530. Even if the "plan" is to extend or even increase them three years from now, it will take the political will of and action by the then current Cabinet. Thus, any such extension can only be seen as uncertain. Such can hardly be encouraging for those considering doing business and investing in Thailand beyond the next three years. Therefore, although the business community is welcoming the CITR reductions under RD 530, it is unfortunate that they were not made "permanent" for all Thai companies."

For more on Duensing Kippen <link>http://www.duensingkippen.com*CLICK</link>

Other News

Read more

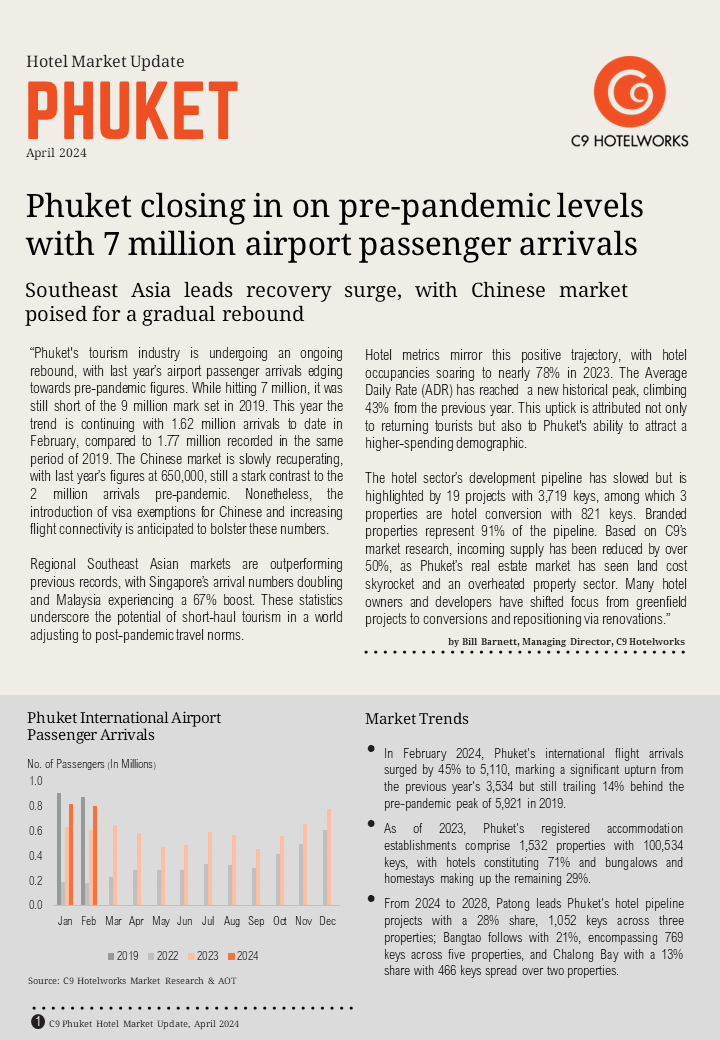

New Phuket Hotel Market Update 2024 Report From C9 Hotelworks

Category: Hotels|Tourism, Posted:17 Apr 2024 | 19:06 pm Phuket’s tourism industry is undergoing an ongoing rebound, with last year’s airport passenger arrivals edging towards pre-pandemic figures according to C9 Hotelwork’s Phuket Hotel Market Update 2024. While hitting 7 million, it was still short of the 9 million mark set in 2019. This year the trend is continuing with 1.62 million arrivals to date […]Read more