Pullman Goes Bleisure

Category:

Hotels, Posted:29 Jul 2013 | 06:00 am

ACCOR's fast expanding Pullman brand is updating their portfolio with a focus new brand symbol and marketing campaign.

After a change in leadership at the top of the chain, the group has said it wants to define its brands with more clarity.

For Pullman the marriage is meant for pairing business and leisure, with a yin-yang inspired focus.

The ACCOR move comes at the same time Marriott have refreshed their core brand under the new "Travel Brilliantly" campaign.

Will these makeover's increase business? They jury is out. but in most cases hotel owners will need to cash up to cover the costs of the updated brand standards.

Other News

Read more

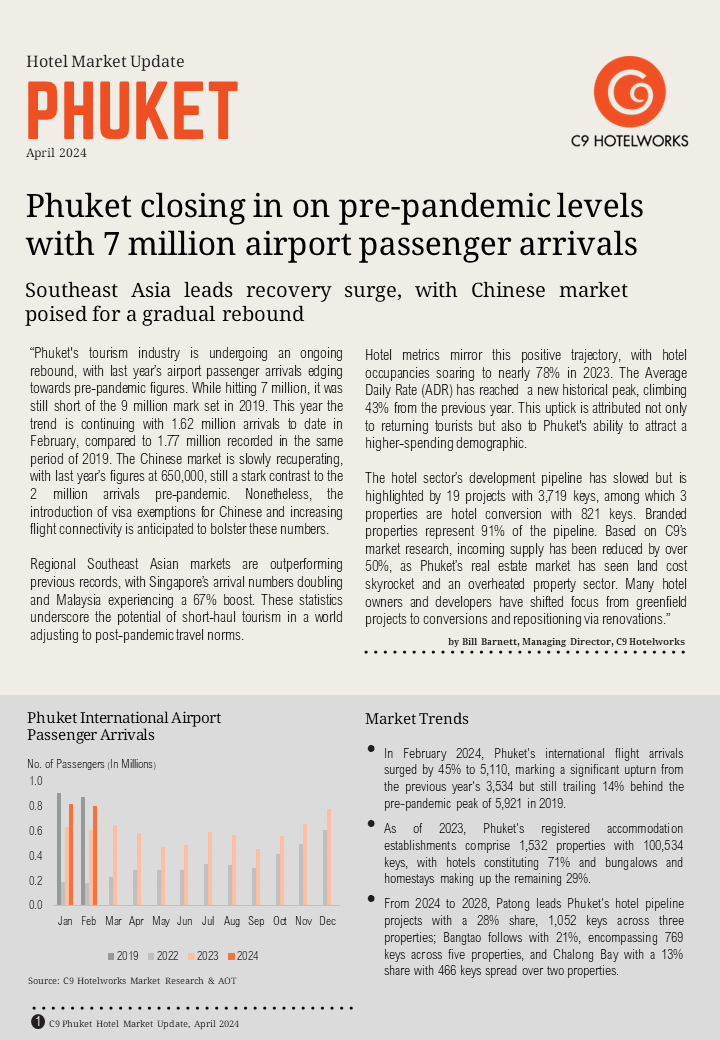

New Phuket Hotel Market Update 2024 Report From C9 Hotelworks

Category: Hotels|Tourism, Posted:17 Apr 2024 | 19:06 pm Phuket’s tourism industry is undergoing an ongoing rebound, with last year’s airport passenger arrivals edging towards pre-pandemic figures according to C9 Hotelwork’s Phuket Hotel Market Update 2024. While hitting 7 million, it was still short of the 9 million mark set in 2019. This year the trend is continuing with 1.62 million arrivals to date […]Read more