The New Phuket

Category:

, Posted:03 Dec 2014 | 11:58 am

Tourism and property set to benefit on the 'New Phuket'

Over the past six months the beaches of Asia's premier resort destination have undergone an extreme makeover. Gone are the endless lines of sun loungers and oceanfront commerce that created obstacles for holidaymakers. For those who haven't visited the island in a while, the changes are nothing short of breathtaking.

Thailand's political events in May gave way to a somewhat expected downturn in lead indicator visitor arrivals, though the impact hit hardest in June when year-on-year numbers dropped 14%. Since that time the trend has slowly reversed on a month by month basis and peak period demand for the upcoming season remains positive.

Talking to Phuket hoteliers, expectations are tempered by what might transpire to be a shortened high season, given broader challenges in the global hotel sector.

Bucking the defined downturn period have been the two strongest growth markets for the island, China and Russia. At the end of the first half of 2014, the two countries accounted for nearly half of international visitors to Phuket and, compared to the same period last year, still surged 6% and 14% respectively. Taking a wider perspective for H1 2014 passenger arrivals to the destination hit an all-time high on a cumulative basis, eclipsing 2.8 million.

Taking a look at the real estate market, the main traction continues to be investment in hotel rental type operations. Take up sales rates in these projects remains at the upper end of the transaction market as can be seen at the Cassia Laguna Phuket, and Amari Residences to name two of the prime movers in the sector.

A number of smaller condominium and pool villa projects have jumped on the band wagon, though buyers need to carefully consider the potential of the property to maintain sustainable rentals after the initial guaranteed return period expires.

There remains a strong mismatch between purchaser expectations and actual performance over a longer period of time both in Phuket and across Asia in nontraditional hospitality led residences.

Another red flag for buyers should be that estates who promote rental returns should have a hotel operating license. In some recent instances in Phuket, developments have stopped rental programs as a result of statutory failures, and real estate investors have been left out in the cold.

While the island's property sector has a strong and demonstrated record, hiring good legal advisers and doing research on local conditions is always the best way to mitigate potential risk.

Though most of the sales activity is currently taking place in the condominium market and low entry point villas, two segments seeing potential growth are resales in the secondary market and an impressive list of new luxury ultra-villas coming shortly.

For resales – as vested currency has shifted over the past few years – some early buyers are willing to cash out at attractive prices.

This leaves a reasonable level of upside for buyers. Putting the property back into the long-term rental market, which has grown in the villa and housing market, is attracting strong recurring yields.

Meanwhile, in the luxury market new projects, such as The Residences at Anantara Layan, Avadina Hills, Mont Azure and the Rosewood Phuket will likely come into the market in a significant manner in 2015. These are expected to induce new demand on a regional and global basis and represent a 'second coming' for Phuket's upscale real estate.

One positive indicator has been a series of secondary sales of multimillion dollar villas in 2014, which points to the fact that the segment has continued to see ongoing demand. At the same time the sell out of Andara Signature, strong transactions at the second Malaiwana project and new trades at Point Yamu by Como all validate the momentum.

Taking a look at 2015, geopolitical events remain on the upswing across the globe, pointing to trading volatility versus the more traditional cyclical trading patterns for both tourism and property. That said, Phuket remains uniquely leveraged within a short radius of emerging markets and also retains the strength of impressive critical mass in the two industries.

If any lessons are to be learned from the events of 2014, it is that the track record between events and recovery has been over a relatively short period and that, on a broader basis, trading fundamentals remain strong for Phuket going into next year.

Other News

Read more

New Phuket Hotel Market Update 2024 Report From C9 Hotelworks

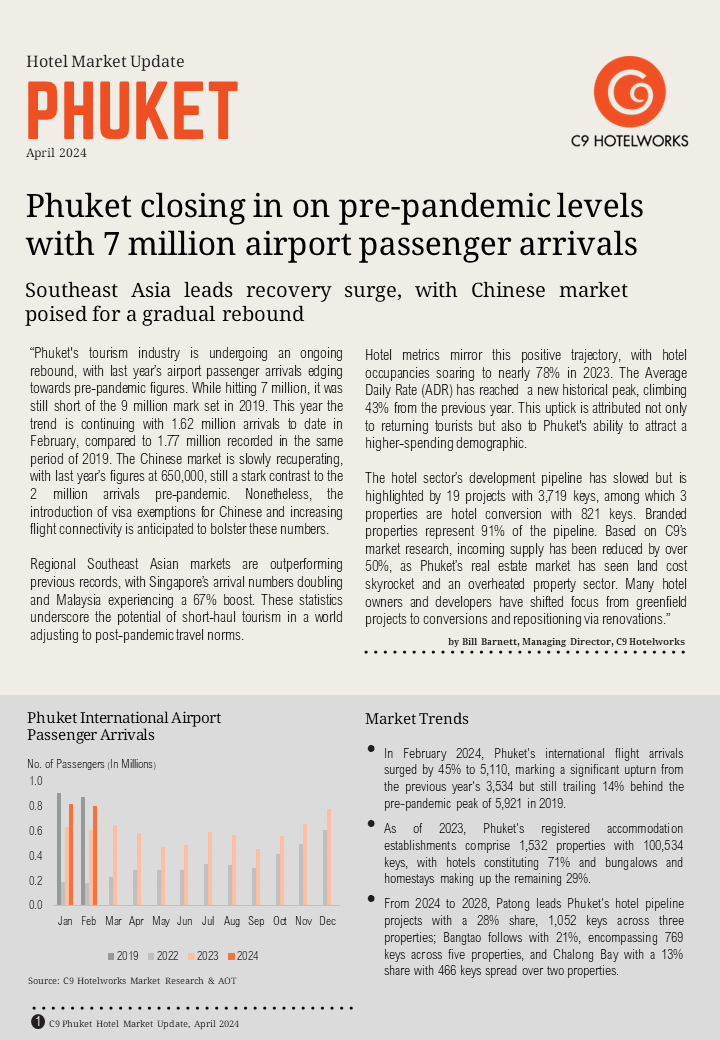

Category: Hotels|Tourism, Posted:17 Apr 2024 | 19:06 pm Phuket’s tourism industry is undergoing an ongoing rebound, with last year’s airport passenger arrivals edging towards pre-pandemic figures according to C9 Hotelwork’s Phuket Hotel Market Update 2024. While hitting 7 million, it was still short of the 9 million mark set in 2019. This year the trend is continuing with 1.62 million arrivals to date […]Read more